A credit score is an important number which is generated by the credit bureaus for the individuals based on their credit habits. It can quietly shape major money decisions in your life. When you apply for a home loan, personal loan, car loan, or even a new credit card in the banks then these banks and NBFCs first check credit score then they work on your loan or credit card papers. A stronger score can improve your chances of approval and may also help you get better interest rates.

Many people only focus on credit score after rejection. A better approach is to understand it early and build healthy habits before you urgently need credit. The good part is that improving your score is possible, even if it has dropped due to past mistakes.

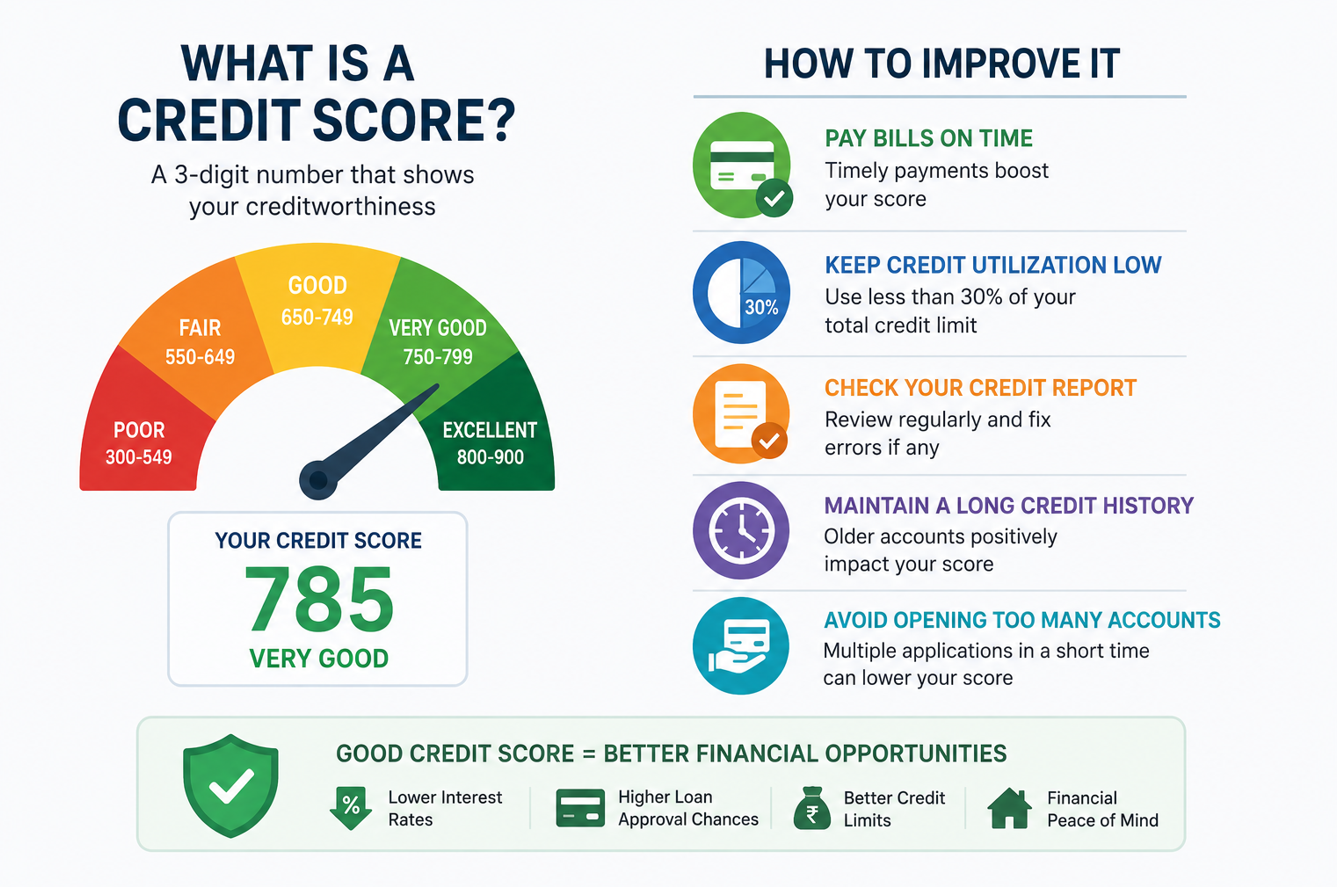

What is a credit score and why does it matter?

A credit score is a three-digit number that shows how responsibly you have handled your previous loans and credit cards. In India, credit bureau scores are commonly seen in a range such as 300 to 900, and generally a higher score signals lower lending risk to banks and NBFCs.

Your score is created using information from your credit history repayment record, loan balances, card usage, length of credit history, recent loan applications, and the type of credit accounts you manage. Banks use this data to estimate how likely you are to repay on time.

Credit score matters and a good score can help with-

- Easier loan approvals

- Better interest rates

- Higher credit card limits over time

- Faster processing in many cases

Whereas a weaker score can lead to rejection, lower limits, or higher interest rate which can lead to higher per month EMI. So, the score is not just about “getting a loan” but it is about the total cost of borrowing (principal and interest) and financial flexibility.

How to improve your credit score in practical steps

The first and most powerful habit is paying your EMIs on time. One late payment or missed payment can bring your score down so to escape from this, you should set auto-debit or reminders for credit card bills and EMIs so deadlines are never missed.

Second, you should keep credit utilization low. If your card limit is Rs 1,00,000 and you usually spend Rs 80,000, lenders may see you as over-dependent on credit. You should keep your credit card usage moderate, and should pay the generated billed amount before the due date whenever possible.

Third, you should avoid applying for many loans or cards in a short period. Multiple hard enquiries can make you appear credit-hungry. You should apply only when needed and when needed, go through all the details in application and fill the details properly.

Fourth, review your credit report regularly. Sometimes it has been found that the loan or credit card is closed from your side but banks have not sent this information to the credit agencies so this appears open at their end. Many times errors happen, such as wrong overdue status or duplicate entries so regular checking (at least once in a year) can avoid any discrepancy from either side. If you spot an issue, raise a dispute with the bureau and banks quickly. A corrected report can improve your score if the mistake was harming you.

Fifth, you should maintain older accounts carefully. Long and stable credit history is usually positive. When you are closing your oldest card without reason then that can reduce your available limit and shorten average credit age.

Finally, keep a healthy mix of credit over time and borrow only what you can repay comfortably. You should always remember that discipline beats shortcuts. There is no instant trick that permanently boosts your score overnight.

In conclusion, your credit score or CIBIL score is a financial trust signal built from everyday behavior in a longer period of time. If you start paying your EMIs on time, control your future utilization, avoid unnecessary borrowing in a very short-short time, and monitor reports regularly, then your credit score can improve steadily. You should start with one habit this month, then build from there and follow other points in time. If you start doing such small but consistent actions then you can create long-term credit strength.

Discover more from Newskart

Subscribe to get the latest posts sent to your email.

Comments are closed.