Buying health insurance often feels overwhelming because every policy sounds “comprehensive” at first glance. But the real difference appears only when a claim is raised. That is why choosing the right plan is less about buying the cheapest premium insurance and more about checking the fine details that decide whether your treatment costs will actually be covered.

If you are selecting a policy for yourself or for your family, then you should think of health insurance as a long-term financial shield. The plan should match your medical risk, city-wise treatment costs, and future needs, not just your current budget.

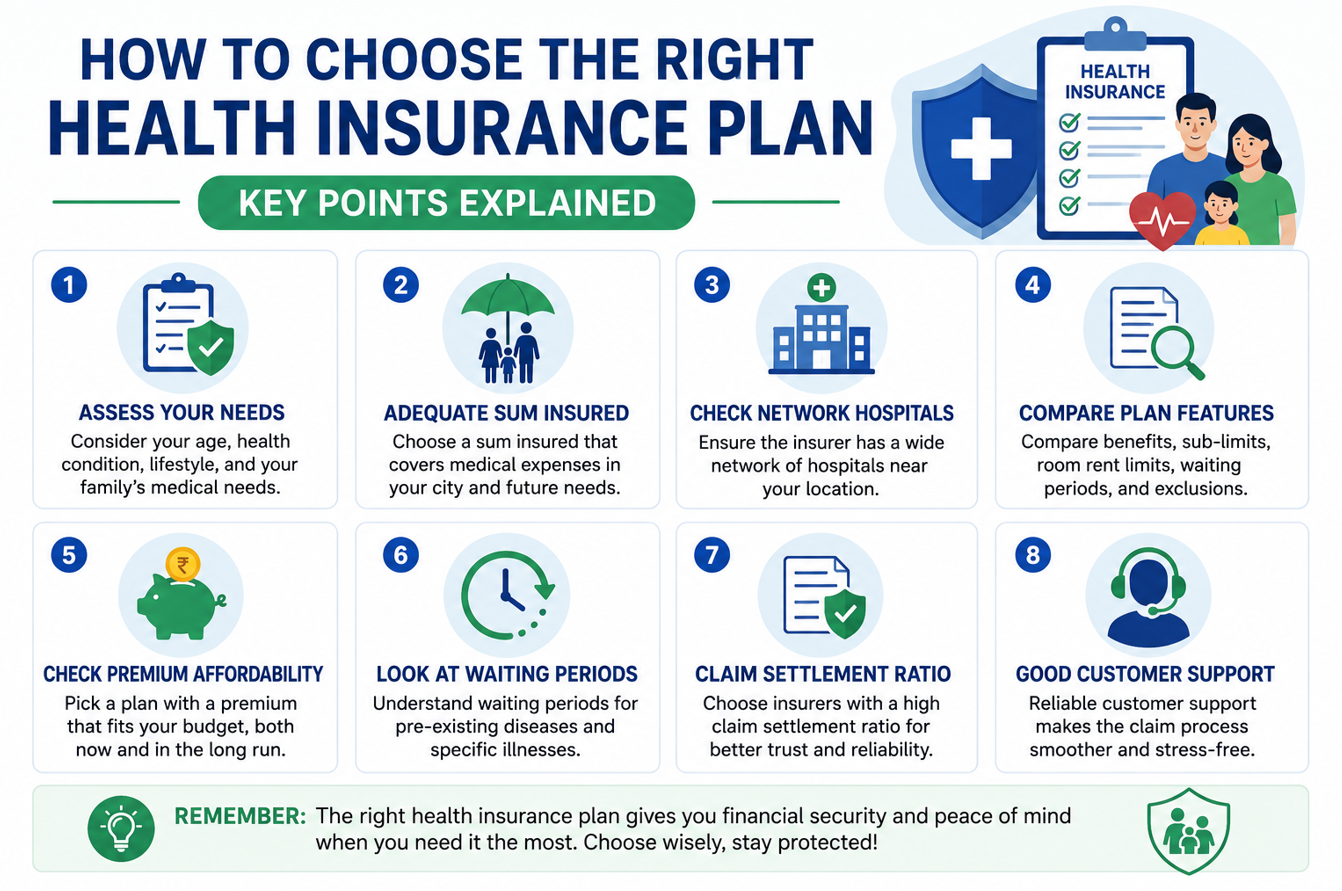

1) Coverage quality- sum insured, inclusions, and exclusions

You should first start with sum insured, because this is the first protection layer which must be at higher side as per your needs. In metro cities, hospitalization costs can rise quickly, so picking a very low cover may create out-of-pocket stress later. If you are buying family floater insurance, choose a limit that can handle one major and one moderate claim in the same year.

Next, you should check what the plan includes. You should compare pre- and post-hospitalization expenses, daycare procedures, ambulance limits, and whether modern treatments are covered. If you compare two different insurance company’s plans with similar premiums then they can differ sharply on these details.

Exclusions are important while purchasing the insurance plan so you must carefully check them. Every policy has conditions it does not cover immediately or fully. Common examples include non-medical consumables, certain procedures, and treatment linked to waiting-period rules. Do not skip this section, because claim disputes often begin here. Also check sub-limits and room-rent caps. A low room-rent cap can indirectly reduce total claim payout due to proportionate deductions on related hospital charges.

2) Waiting periods, network hospitals, and claim process

Waiting period is one of the most important points while choosing a health plan. There may be an initial waiting period for non-accidental claims, plus longer waits for specific illnesses and pre-existing diseases. Policies differ, so compare these timelines side by side before deciding. Best insurance plans are those which cover everything immediately or after 30 days after purchasing the policy.

If you already have a medical condition, look for clarity on pre-existing disease coverage timelines and whether the policy allows portability benefits from previous coverage. Continuity benefits can make a major difference if you switch insurers later.

Now coming to cashless treatment. A large network hospital list is useful only if strong hospitals near your home and workplace are included. These list may vary from company to company but mostly major hospitals are included in such plans for cashless treatment.

3) Long-term fit: renewability, cost trend, and service quality

A good policy should remain useful for years, not just one policy term. So you should check lifetime renewability, no-claim bonus structure, and how premiums typically change with age bands.

Do not select a plan purely on “lowest premium today.” A slightly higher premium with better claim support, broader hospital access, and fewer restrictive conditions may offer better value over time. Before finalizing, compare at least three plans using the same checklist such as sum insured, waiting periods, exclusions, hospital network, claim process, and renewability terms. This side-by-side approach prevents impulse decisions.

Now a days, there are many aggregators sites which provide better comparison window and also offer their expertise to choose the best insurance plans.

In conclusion, the right health insurance plan is the one that performs well during a real medical event, not the one that looks attractive in an ad. If you check coverage depth, waiting-period rules, and claim reliability before purchase, you can protect both your health and your savings with greater confidence.

Discover more from Newskart

Subscribe to get the latest posts sent to your email.

Comments are closed.