UPI Achieves 22.35 Bn Transaction Count in April 2026, Is India Embracing Digital Payments?

If there is one number that captures India’s payment shift this year, it is this – 22.35 billion UPI transactions in April 2026. That is not just a number but it is a sign of how deeply digital payments have entered everyday life, from metro grocery stores to village kirana shops.

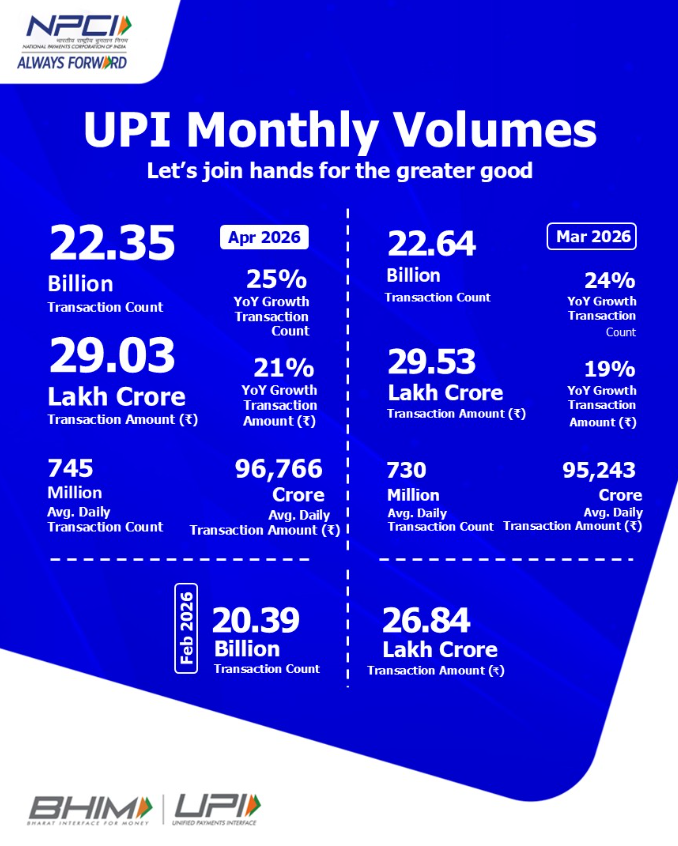

The interesting part is that this came right after a very high March. So even with a small month-on-month softening from March’s peak, the April number stayed massive and showed strong year-on-year growth. In simple words, India is not just experimenting with digital payments anymore. It is building daily life around them.

What the 22.35 Billion Figure Really Means

As reported on 4 May 2026 by official updates of DFS and NPCI, UPI recorded about 22.35 billion transactions in April 2026. Compared to the same month last year, this reflects strong growth. It also follows March 2026, which had set an even higher monthly benchmark.

People often ask, if April is slightly lower than March, is growth slowing? Not really. Month-to-month movement can happen due to billing cycles, holiday patterns, and business payment behavior. What matters more is the trend line across quarters and years, and that line is still moving upward.

Another key point is scale across use cases. UPI is no longer only for peer-to-peer transfers. It now powers:

- daily retail spends,

- utility bill payments,

- food and mobility payments,

- and many merchant settlements across small and large businesses.

This widening usage base is what makes the system resilient even when one category slows briefly.

Is India Truly Embracing Digital Payments?

Short answer: yes, but with some important layers.

India is clearly embracing digital payments in behavior. Consumers trust QR payments for low-ticket transactions, and merchants accept them because settlement is fast and setup cost is low. Even users who keep cash as backup now treat UPI as default for routine spending.

However, “embracing” does not mean “cash has disappeared.” Cash still plays a role in many geographies and user groups. What has changed is hierarchy, for many urban and semi-urban users, UPI is first choice and cash is second.

The bigger achievement is inclusion and interoperability. UPI works across banks, apps, and merchant sizes. That reduces friction and increases confidence. A user does not need to worry about matching wallet platforms or specific bank branches. This “works-everywhere” experience is a major reason adoption keeps rising.

For businesses, especially small merchants, digital trails can improve access to formal credit over time. For governments and policy makers, digital transactions improve transparency and efficiency. For users, convenience is obvious, less cash handling, quick settlement, and easy records.

What to Watch Next

The next phase is about quality, not just quantity. India’s digital payment story will now be judged on:

- fraud control and user safety,

- uptime reliability at very high transaction loads,

- feature access for low-connectivity users,

- and deeper adoption in smaller towns without usability drop.

If these improve alongside volume growth, then the digital payments shift becomes structurally stronger-not just a headline milestone. So, is India embracing digital payments? The 22.35 billion April number strongly says yes. But the bigger success will be measured by how secure, inclusive, and dependable this ecosystem remains as usage scales even further.

Discover more from Newskart

Subscribe to get the latest posts sent to your email.

[…] current technology story is strongest in digital public infrastructure and large-scale adoption. UPI continues to operate at massive scale, with official updates in early May 2026 highlighting over 22 […]